For decades, the promise of digital transformation was meant to revolutionize how goods flow from raw materials to the end consumer. Yet, beneath the veneer of modern enterprise software and high-level corporate strategies, a sobering reality has emerged: 82% of industries are seeing their supply chain performance move backward. As companies scramble to implement the latest AI-driven optimizations, they are often fighting an uphill battle, unaware that their foundational models are fundamentally mismatched with the realities of their specific sectors.

The industry is suffering from a "leadership vacuum," where the focus has been on automating outdated processes rather than rethinking the value network. To drive meaningful change, supply chain leaders must abandon the "one-size-fits-all" spreadsheet mentality and embrace the unique operational requirements of their specific markets.

The Myth of Scale and the Spreadsheet Trap

Many supply chain consultants and technology providers operate under the dangerous assumption that supply chain management is a universal discipline. They attempt to force diverse corporate structures into rigid spreadsheets, effectively stripping away the industry-specific nuances that define competitive advantage. This homogenization is a fatal error.

According to the latest "Supply Chains to Admire" analysis—a comprehensive research project that has tracked industry patterns over a ten-year horizon (2016–2025)—the reliance on generalized methodologies has led to a stagnation in supply chain economies of scale. Contrary to the popular belief that larger companies possess an inherent advantage, the data reveals a different story: smaller, innovation-focused companies consistently outperform their massive, established peers.

For instance, companies like Church & Dwight are outperforming Procter & Gamble, while Monster Beverages is achieving results that dwarf the metrics of industry giants like AB InBev, Coca-Cola, and PepsiCo. Similarly, Ecolabs is demonstrating superior efficiency compared to industrial titans like BASF and Dow. These findings suggest that the quest for massive scale has often come at the expense of agility and operational precision.

Chronology of a Decade: The Impact of Global Disruption

The "Supply Chains to Admire" report, which requires an intensive 22-week process of data gathering and analysis, offers a rare, longitudinal look at how global events have reshaped the supply chain landscape. By comparing the three-year period preceding the COVID-19 pandemic with the three years following it, researchers have gained profound insights into the nature of organizational resilience.

Pre-COVID: The Era of Steady Growth

Before 2020, the typical manufacturing company experienced a modest, yet consistent, annual growth rate of approximately 2.8%. During this period, the focus was largely on refining existing "make-to-stock" processes, particularly in the process-based manufacturing sector.

Post-COVID: A Tale of Two Sectors

The pandemic served as a catalyst for a massive divergence between two primary manufacturing archetypes:

- Process-Based Manufacturing: Predominantly focused on "make-to-stock" processes, these companies—with the notable exception of the pharmaceutical sector—have largely stalled in the post-pandemic years.

- Discrete Manufacturing: Companies focused on "configure-to-order" or "make-to-order" processes saw a significant rebound. Driven by geopolitical shifts, rapid technological adoption, and the explosion of Artificial Intelligence, the discrete sector has demonstrated an ability to adapt that their process-based counterparts have yet to mirror.

The report notes that technologists have historically prioritized the automation of process-based industries, leaving the discrete sector underserved despite its massive market potential.

Data-Driven Performance: Measuring Value over Cost

To understand why some companies thrive while others falter, the "Supply Chains to Admire" report evaluates performance at the intersection of operating margin and inventory turns. By analyzing growth, inventory turns, operating margin, and Return on Capital Employed (ROCE), the research identifies a clear correlation with market capitalization per employee.

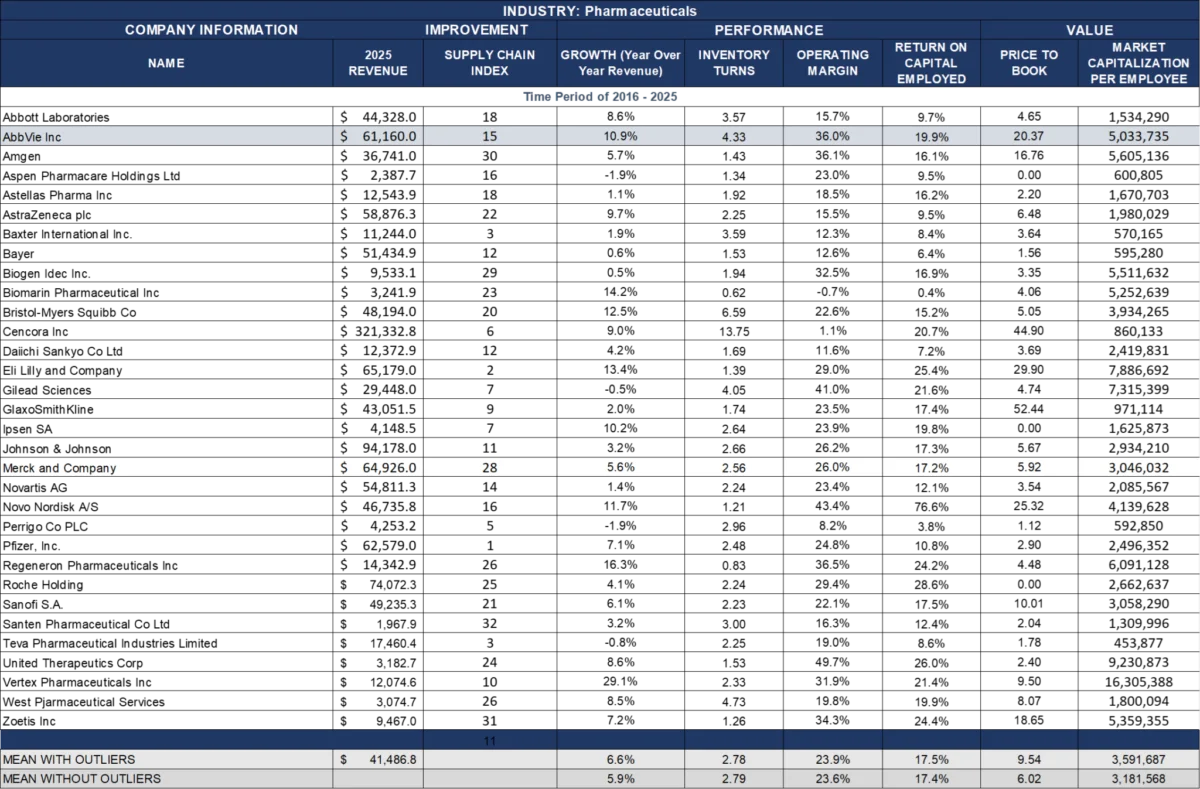

This metric is vital because it shifts the focus from a traditional "cost-based" agenda to a "value-driven" one. The analysis reveals that the highest-performing sectors—including beverages, household durables, medical devices, pharmaceuticals, and semiconductors—all share a common trait: they have successfully aligned their supply chain operations with their specific market demands.

The Medical Device Dilemma

A prime example of the current disconnect is the medical device industry. While it maintains an impressive 19.1% operating margin, its supply chain performance saw a steady decline from 2016 to 2023. The root cause? A reliance on manual processes for critical inbound supply chain functions, such as procurement and manufacturing. While a rebound began in 2023, the industry still faces significant hurdles in lineage and quality of conformance. The sector serves as a cautionary tale: high margins can mask fundamental inefficiencies that, if left unaddressed, will eventually erode competitive standing.

The Leadership Vacuum and the AI Trap

Perhaps the most alarming finding is the lack of initiative among industry leaders. Currently, no company with an operating margin above 15% has taken the lead in building a true "value network" or cracked the code on network interoperability. Despite forty years of technological advancement, the backbone of the global supply chain remains a fragile patchwork of spreadsheets and Electronic Data Interchange (EDI).

There is a growing fear among industry experts that the current rush to integrate Artificial Intelligence into existing supply chain systems will only exacerbate these issues. Many technology marketers are currently pushing "agent-based" solutions designed to sit on top of legacy Advanced Planning Systems (APS) or Enterprise Resource Planning (ERP) software.

"I am fearful that we will put AI on top of a system that requires fundamental change," says the lead researcher of the report. Applying advanced AI to a system built on flawed, manual, or siloed foundations will not create an autonomous supply chain; it will merely automate the chaos at a faster rate.

Strategic Implications: Building the Value Network

For supply chain leaders, the path forward is clear but demanding. It requires a fundamental shift in how organizations view their position within the value chain.

1. Shift from Enterprise to Network

Companies must stop trying to optimize their own internal enterprise systems in isolation. The future lies in building "value networks"—interoperable ecosystems where data flows seamlessly between partners, suppliers, and customers. This requires moving beyond the "enterprise-centric" model that has dominated the last two decades.

2. Prioritize Industry Nuance

Leadership teams must reject generalized technology solutions that lack industry-specific functionality. Whether a company is in discrete manufacturing or process-based production, the underlying software and operational strategies must respect the nuances of their specific "configure-to-order" or "make-to-stock" requirements.

3. Focus on Value, Not Just Cost

The goal of supply chain transformation should not merely be cost reduction. As the research indicates, the metrics that truly predict long-term market value are those that measure efficiency, agility, and return on capital. Leaders must champion a strategy that treats the supply chain as a strategic asset for growth, not a cost center to be squeezed.

4. Address the Manual Bottlenecks

The analysis of the medical device industry proves that even highly profitable sectors are prone to "hidden" manual processes. Organizations must perform a cold-eyed audit of their inbound supply chain to identify where manual labor is impeding lineage and quality control.

Conclusion: A Call to Action

The data is unequivocal: the era of relying on legacy practices and bloated enterprise software is coming to a close. The "Supply Chains to Admire" report serves as both a diagnostic tool and a call to arms. For the 82% of industries currently experiencing a decline in performance, the time for "business as usual" has expired.

As we look toward the remainder of the decade, the winners will be those who resist the urge to simply layer AI over broken processes. Instead, they will be the companies that embrace the complexity of their specific industry, build robust and interoperable value networks, and prioritize long-term value over short-term cost savings. The technology is available, but the leadership—and the courage to fundamentally change—must come from within.