The American freight landscape is currently navigating a period of unprecedented volatility, characterized by the convergence of a long-standing capacity correction and a transformative legal development from the U.S. Supreme Court. While industry participants have been focused on the slow, grueling recovery from a multi-year freight recession, the recent ruling in Montgomery v. Caribe Transport II, LLC has introduced a new, inflationary variable into the pricing equation. As freight brokers and shippers grapple with the implications of this decision, the trucking industry is poised for a structural shift in how risk is priced, managed, and passed down the supply chain.

The Supreme Court’s Pivot: A New Legal Reality for Brokers

The Supreme Court’s decision to rule against freight brokers in the Montgomery case represents a watershed moment for the logistics sector. Historically, the role of a freight broker has been defined by a relatively narrow scope of liability. Under the existing framework, brokerages were generally shielded from the primary liability associated with the carriers they hired, provided they operated within the bounds of their role as intermediaries. Their financial exposure was traditionally capped by a $75,000 surety bond, intended primarily to cover payment defaults rather than catastrophic injury or property damage.

In contrast, asset-based carriers have long operated under a mandate to maintain significant insurance coverage, typically including $1 million in auto liability and $100,000 in cargo coverage per load. The Montgomery ruling effectively collapses the legal distance between the broker and the carrier in cases of accidents. By enabling accident victims to pursue litigation against the brokerages that facilitate the hire of the involved carrier, the court has signaled an end to the "intermediary shield" that has defined the brokerage business model for decades.

For the brokerage community, this is not merely a legal nuisance; it is an existential challenge. Brokers must now grapple with the ambiguous, high-stakes standard of "reasonable care" in carrier vetting. The ambiguity of this standard is what keeps industry legal teams up at night. What constitutes a "reasonable" investigation into a carrier’s safety record, maintenance standards, and financial stability? As the courts begin to interpret this standard, brokers will inevitably gravitate toward safer, more expensive, and more established carriers, effectively pricing out the smaller, lower-cost owner-operators who have historically provided the "spot market buffer" during tight capacity windows.

Chronology: From Recession to Regulatory Shock

To understand the current market tension, one must look at the timeline of the freight recession and the recent surge in demand.

- 2022–2024 (The Great Correction): Following the pandemic-driven surge in consumer demand and the subsequent inventory glut, the freight industry entered a prolonged recession. Excess capacity in the form of small carriers—who flooded the market during the boom—began to exit as spot rates plummeted.

- April 2025 – Q1 2026: Market data from SONAR began showing a consistent upward trajectory in contract rates. This was not necessarily a reflection of primary carriers hiking prices, but rather a reflection of "route guide failure." As primary carriers rejected loads, shippers were forced to move freight to secondary and tertiary providers, driving up the "effective cost" of freight for shippers.

- May 14, 2026: The conclusion of the annual Roadcheck safety event marked a turning point. As industry focus shifted to compliance and safety, tender rejection rates hit new highs. Spot rates responded with a sharp 5.7% jump in just three days, signaling that the market was already "tight" before the legal shockwaves began to fully register.

- Late May 2026: The Montgomery v. Caribe Transport II, LLC ruling lands. The industry is currently in the "digestion phase," where brokers, insurance underwriters, and legal departments are assessing the total cost of the new liability burden.

Analyzing the Data: The Widening Spread

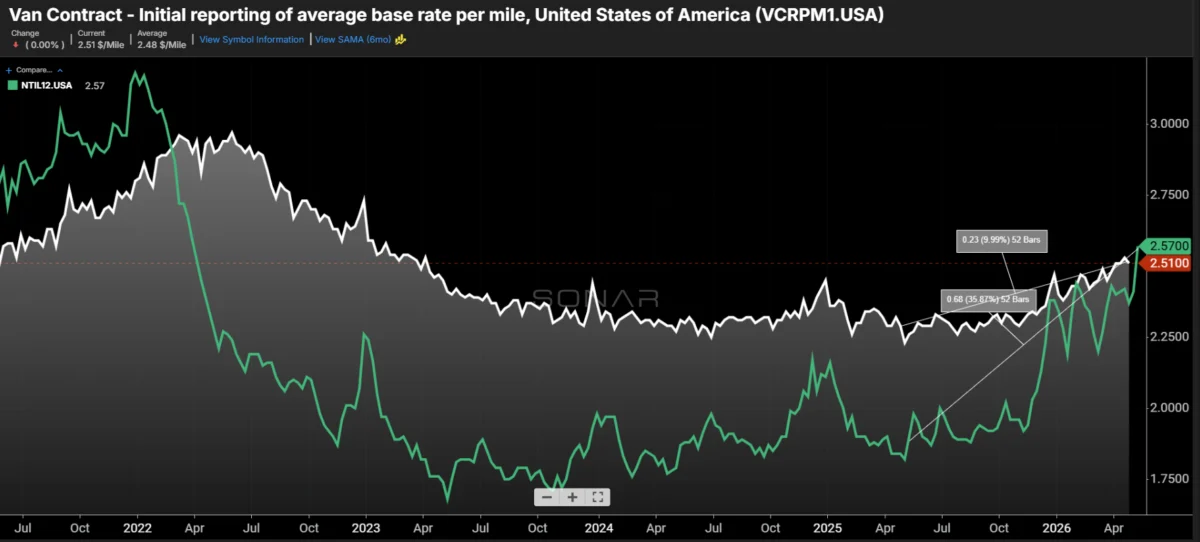

The relationship between contract and spot rates provides the clearest window into the current market tightening. According to data from the National Truckload Index (NTIL12) and the Van Contract Rate Index (VCRPM1), the market is undergoing a fundamental realignment.

Contract rates have risen by approximately 10% since April of the previous year. However, this figure is deceptive. It masks the reality that shippers are paying much more in "payables" because their primary, lower-cost contract carriers are failing to accept loads, forcing shippers into more expensive, non-contract, or secondary-provider arrangements.

Spot rates have been even more volatile, with year-over-year increases ranging between 35% and 40%. The spot market is the most exposed segment of the supply chain because it is driven almost entirely by the rapid-fire negotiations of 3PLs and freight brokers. With the Montgomery ruling, the risk premium on every spot load is about to skyrocket. Brokers, now facing potentially unlimited liability for the carriers they dispatch, are no longer just buying "trucks"; they are buying "risk-mitigated capacity."

In 2023, spot rates sat at a 25–30% discount to contract rates. That spread is rapidly narrowing. As brokers demand higher safety thresholds to protect themselves from lawsuits, the "cheap" segment of the spot market—often dominated by carriers with limited history or spotty safety data—will find it increasingly difficult to secure loads. This reduction in the pool of eligible carriers will naturally exert upward pressure on rates, regardless of seasonal demand.

Implications: An Inherently Inflationary Future

The ultimate consequence of this regulatory shift is, by every metric, inflationary. The industry is witnessing a "double-squeeze" on logistics costs.

1. The Insurance and Legal Tax

Brokerages will be forced to renegotiate their insurance policies. Insurance providers, aware of the new, massive liability exposure for brokers, will raise premiums across the board. These costs cannot be absorbed indefinitely by the brokers; they will be passed down to the shippers in the form of higher brokerage fees and, eventually, higher freight rates.

2. The Narrowing of the Carrier Base

The "reasonable care" standard effectively acts as a filter. Brokers will likely drop carriers who do not meet rigorous, and often costly, safety criteria. This reduces the total available supply of trucks. In the basic economics of supply and demand, a reduction in the supply of capacity while demand remains stable or increases—as is typical in the summer months—will lead to sustained rate elevation.

3. The End of "Low-Cost" Spot Freight

For years, the spot market was the go-to for shippers looking to minimize costs. That era is effectively over. The risk premium associated with hiring an unvetted or low-cost carrier now far outweighs the savings. Shippers will have to prepare for a "new normal" where the price of shipping is tethered not just to fuel and demand, but to the legal cost of risk mitigation.

Looking Ahead: A Market in Transition

While the immediate impact of the Montgomery ruling is being exacerbated by the seasonal surge in freight following Roadcheck, the long-term structural changes will take months, if not years, to fully stabilize. We are entering an eight-week stretch of traditionally high shipping activity and holiday-related disruptions. During this time, the market will likely see the full brunt of the "regulatory inflation" as brokers struggle to balance their new liability burdens with the immediate need to move freight.

The industry must now prepare for a period of institutional re-evaluation. Large-scale brokerages will likely implement advanced, AI-driven carrier vetting systems to meet the "reasonable care" threshold. Smaller brokerages, unable to afford the insurance premiums or the legal infrastructure required for this new environment, may face consolidation or closure.

Ultimately, the Montgomery ruling has served as a catalyst for a market that was already trending toward tighter capacity and higher costs. The "cheap" freight market is vanishing, replaced by a more disciplined, risk-averse, and expensive ecosystem. For shippers, the lesson is clear: in an era of heightened liability, reliability and safety are no longer just operational metrics—they are the primary drivers of the cost of doing business. As the market moves through the remainder of 2026, participants should expect that while seasonal volatility will eventually settle, the inflationary pressure introduced by this legal paradigm shift is here to stay.