The modern food industry is currently reckoning with a "lost decade." When analyzing the performance metrics of the sector from 2016 through 2025, the primary reaction among industry analysts is one of profound alarm. Despite the rapid advancement of digital technology, the global food industry has witnessed a precipitous decline in operational efficiency and supply chain performance. This stagnation is not the result of external forces alone; it is a crisis of philosophy, fueled by a stubborn refusal to abandon outdated paradigms.

The Chronology of Decline: A Decade of Misalignment

The period between 2016 and 2025 serves as a cautionary tale of institutional inertia. At the start of this window, the industry was still riding the momentum of 1990s-era "best practices." Executives, bolstered by the success of the previous century, clung to these methodologies—namely, the reduction of demand error, the relentless "sweating" of manufacturing assets, and the heavy outsourcing of product launches.

However, as the market evolved, these practices became increasingly detrimental. By 2018, the rise of e-commerce and changing consumer preferences toward health-conscious, localized sourcing began to fracture the traditional "one-size-fits-all" supply chain. Rather than pivot, industry leaders doubled down on cost-cutting. The pandemic-era disruptions of 2020–2022 further exposed the fragility of these systems, yet the industry’s response was merely to layer new, complex AI-driven tools over broken, legacy foundations. By 2025, with major inflationary spikes in protein—specifically beef and eggs—and widespread disease-related supply shortages, the industry found itself caught in a cycle of volatility from which it has yet to emerge.

Supporting Data: The Erosion of Operational Excellence

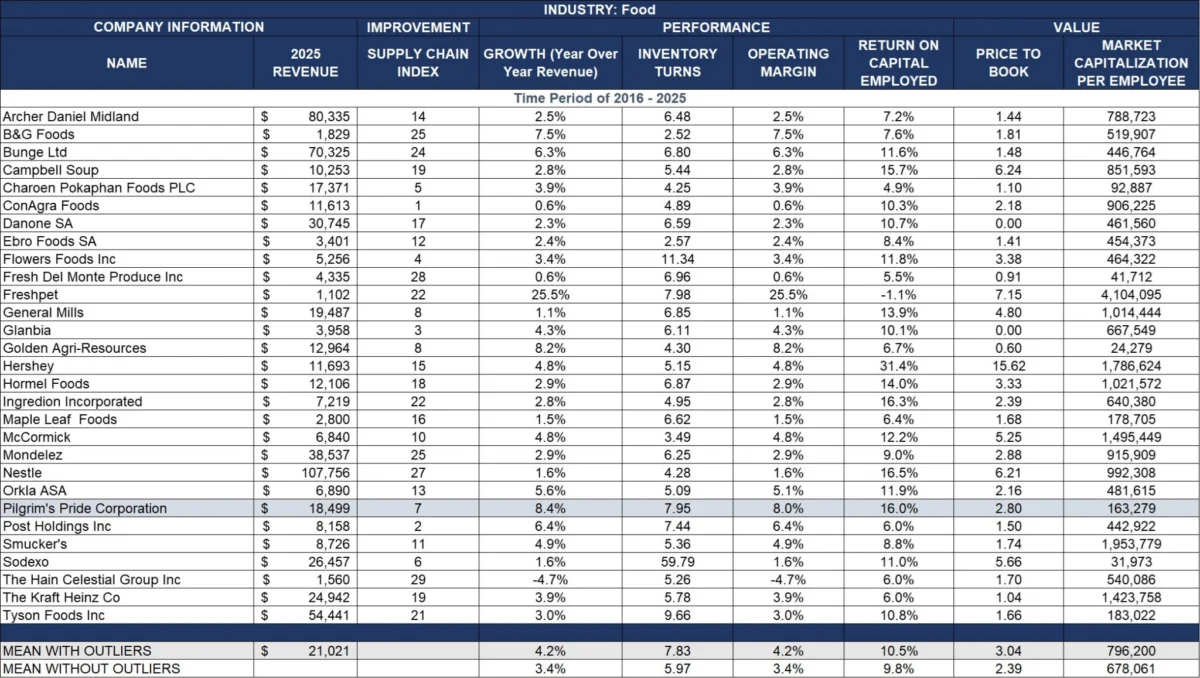

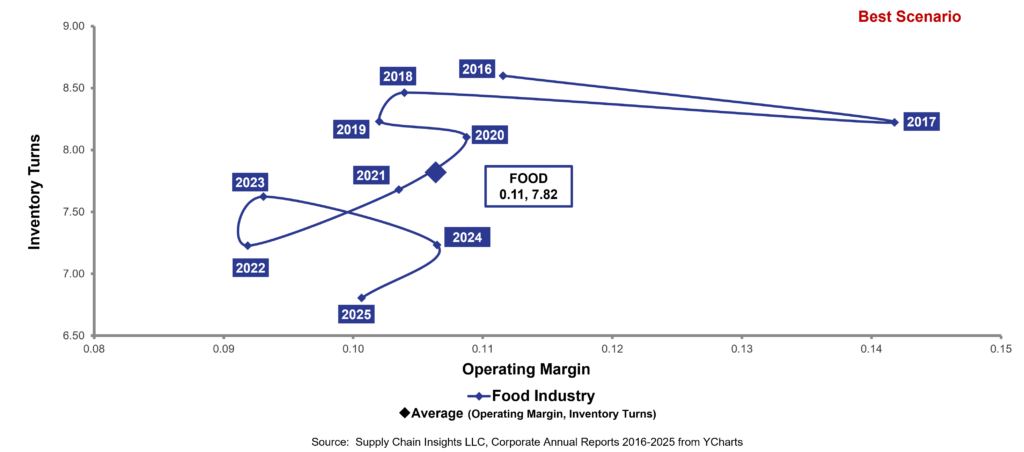

The data between 2016 and 2025 paints a sobering picture of inefficiency. During this decade, the industry maintained an average operating margin of 11% and 7.82 inventory turns. While these numbers might appear stable in isolation, the deeper trends reveal a 35% decline in inventory performance efficiency.

The industry’s "inside-out" focus—prioritizing internal manufacturing metrics like Overall Equipment Effectiveness (OEE) over market signals—has created a widening gap between production and demand. Consider the following key performance indicators:

- Order Latency: The time elapsed between shelf take-away and the generation of a replacement order has increased by 15% to 20%. This delay has effectively blinded manufacturers to real-time shifts in consumer behavior.

- Inventory Bloat: Despite high demand for agility, the industry has become burdened by the "long tail" of products—unforecastable items that clog the supply chain and intensify the bullwhip effect.

- The Consolidation Paradox: Major conglomerates like Kraft/Heinz and Mondelez, which relied on aggressive consolidation to drive efficiency, ultimately saw their performance suffer. Their mandate to cut costs effectively stifled the agility required to manage the 85% of their product volume that does not fit into a lean, low-cost operational model.

The Anatomy of Failure: Why Big Brands Underperformed

The performance gap between industry titans and smaller, more nimble competitors has reached an inflection point. Large-scale manufacturers—including Campbell’s, General Mills, Hershey, and Nestle—have consistently underperformed against smaller or more specialized entities like Pilgrim’s Pride.

The reasons for this are structural:

1. The Trap of "Efficiency-First" Management

Many large organizations fell victim to the belief that the "best supply chain is an efficient supply chain." This mantra, often pushed by financial ownership groups, ignores the reality of modern complexity. Only a small fraction of a company’s volume can be managed through pure, high-volume efficiency. The remaining majority requires an agile, responsive network. By forcing a low-cost agenda across the entire portfolio, these companies effectively hollowed out their own operational expertise.

2. Marketing-Driven vs. Market-Driven Strategy

The industry has largely moved away from being "market-driven" (listening to the consumer) to "marketing-driven" (pushing products regardless of supply chain viability). This has led to an unchecked expansion of item complexity. As product lists grew, the ability to accurately forecast demand diminished. Procurement teams, operating in silos, focused on reducing manufacturing costs rather than optimizing the bi-directional orchestration of trade-offs between procurement, manufacturing, and logistics.

3. The Failure of Functional Metrics

Companies like Kellogg’s serve as a case study in the danger of prioritizing functional metrics over holistic value. By pushing factories to their absolute limits to satisfy OEE targets, the company saw its costs soar while sales volumes remained stagnant. This misalignment eventually led to leadership turnover and the eventual sale of the company at a discounted valuation.

Official Responses and Industry Sentiment

While no single entity has publicly accepted blame for the sector’s performance decline, the consensus among industry consultants and private equity firms is clear: the "old guard" is failing.

Current leadership within major food corporations often points to global inflation and supply chain volatility as the primary culprits for poor margins. However, experts argue that these are merely symptoms of an underlying failure to adapt. The lack of meaningful point-of-sale (POS) data integration is a recurring theme. Even today, very few companies are successfully leveraging market data to drive decision-making. Instead, the industry is caught in a trap of "digital theater"—buying expensive AI software and layering it over manual, outdated processes, which serves only to accelerate the speed of the failure.

Implications: The Path Toward Agility

The implications of this decade of decline are profound. The food industry is currently at a crossroads. The rise of private equity-backed "challenger brands"—which prioritize fresh ingredients and localized, agile supply chains—proves that the consumer is willing to pay for quality and availability.

Redefining the Supply Chain

To recover, the industry must fundamentally change its approach:

- From Inside-Out to Outside-In: Companies must move away from manufacturing-centric KPIs and begin measuring demand shaping and real-time consumption data.

- Demand-Driven Orchestration: Procurement must be re-integrated into the broader supply chain strategy. Decisions regarding manufacturing must be made in tandem with procurement, rather than as a separate, cost-focused silo.

- Embracing Complexity: Instead of trying to force all products into a high-efficiency model, companies must categorize their portfolio. High-volume, stable goods can remain efficient; however, the "long tail" of products requires a separate, agile supply chain that can respond to volatility without disrupting the entire organization.

Final Thoughts: The Need for Radical Adaptation

The fall of the food industry’s supply chain performance is more than a fiscal issue; it is a failure of vision. As we look beyond 2025, the focus on "autonomous supply chains" must be tempered with the realization that automation cannot fix a flawed process.

The industry has spent years focusing on cheaper ingredients to maintain margins, but the real waste lies in the outdated, rigid processes that prevent these companies from reaching their customers effectively. The success of smaller brands demonstrates that the market is ready for a change. It is time for the food industry to stop clinging to the "good old days" and start building a supply chain designed for the volatility of the future. The question is no longer whether they can afford to change—it is whether they can afford not to.