Three years ago, the pursuit of Financial Independence, Retire Early (FIRE) was often hampered by a lack of sophisticated, accessible analytical tools. Most financial calculators were static, binary, and failed to account for the complex tax nuances inherent in early retirement. That changed with the emergence of ProjectionLab, a platform that quickly distinguished itself as the gold standard for high-net-worth individuals and FIRE enthusiasts alike.

Today, ProjectionLab has moved beyond being a simple calculator. Following two years of intensive, full-time development, the platform has transformed into a robust, automated financial architect capable of optimizing multi-decade wealth strategies. With over 200,000 households currently using the software to map their financial futures, the tool is setting a new benchmark for how individuals approach tax planning, asset drawdown, and legacy building.

A Chronology of Growth: From Side Project to Industry Disruptor

The story of ProjectionLab is a testament to the power of community-driven development. When Kyle, the project’s founder and lead developer, first introduced the tool, he was navigating the traditional path of a corporate career. ProjectionLab was a labor of love—a project developed in the quiet hours of nights, weekends, and holidays.

The Feedback Loop

The initial launch served as a catalyst. The Mad Fientist community, known for its rigorous approach to tax avoidance, Roth conversions, and discretionary withdrawal strategies, provided immediate, high-level feedback. This was not just "user feedback" in the traditional sense; it was a collaborative effort to bridge the gap between financial theory and software execution.

"The Mad Fientist community helped change the trajectory of this project," Kyle notes. "They gave me the confidence to bet my career on it."

Scaling the Vision

The trajectory was rapid. Two months after the initial surge of interest, Kyle transitioned to part-time work. Within six months, he left his corporate position entirely to focus on building the platform. Unlike many Silicon Valley startups, ProjectionLab has remained a staunchly independent, profitable entity. By eschewing venture capital, advisory upsells, and the commodification of user data, the team has maintained a user-centric development cycle that prioritizes utility over profit-maximizing dark patterns.

The Technological Leap: Why Modern Planning Requires Automation

The traditional model of financial planning—relying on a spreadsheet or a basic online calculator—is increasingly obsolete for those aiming for complex, long-term financial independence. The modern retiree faces a "tax minefield" that includes IRMAA surcharges, ACA subsidy cliffs, and the delicate balancing act of Roth conversions.

The Power of the Optimizer

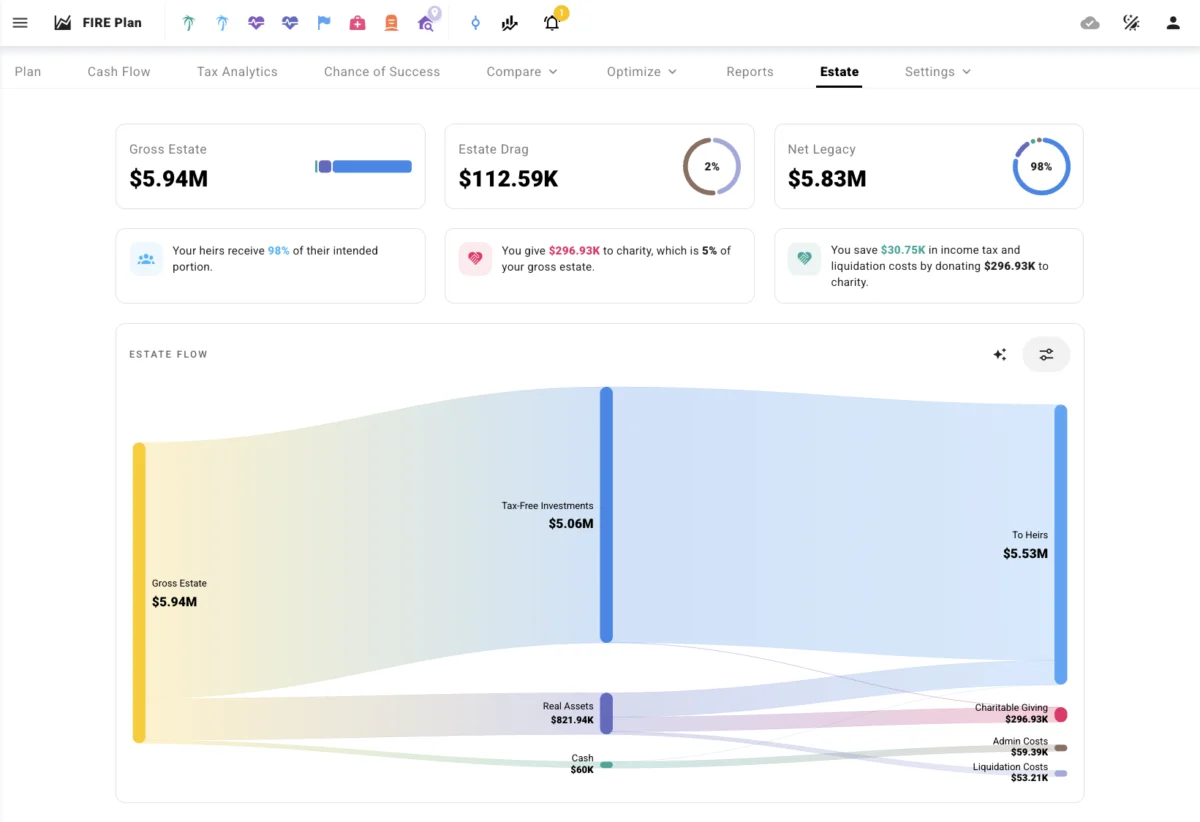

At the core of the new ProjectionLab is the "Optimizer." This engine functions as an automated fiduciary. Instead of forcing users to guess which tax bracket they should target, the Optimizer scans hundreds of permutations of tax strategies to find the one that best aligns with the user’s goals—whether that goal is minimizing lifetime tax liability, maximizing legacy value for heirs, or ensuring a specific net worth threshold.

This level of analytical depth was once exclusively the domain of high-fee financial advisors. By democratizing this logic, ProjectionLab allows users to conduct "what-if" analyses that would take a professional hours to manually compute.

Deep Dive: Key Features and Advanced Capabilities

The recent updates to ProjectionLab represent a significant leap in functional depth. The following features address the most common failure points in retirement planning:

1. Advanced Tax Strategy and Optimization

Tax efficiency is the single greatest lever in long-term wealth preservation. ProjectionLab now automates the identification of optimal tax brackets. It accounts for:

- Federal Tax Brackets: Real-time adjustments based on income and filing status.

- IRMAA Thresholds: Managing income to avoid Medicare premium surcharges.

- ACA Subsidy Limits: Strategic income management to ensure eligibility.

- The NIIT Cliff: Mitigating the Net Investment Income Tax.

2. Intelligent Roth Conversions and Drawdown

A common error among early retirees is the "lumpy" income profile, where a lack of strategic planning leads to massive tax bills in later years due to Required Minimum Distributions (RMDs). ProjectionLab’s engine is "IRMAA-aware," meaning it will execute Roth conversions to fill target brackets without triggering future penalties. Similarly, the drawdown engine manages the sequence of returns by intelligently pulling from accounts in an order that optimizes for current and future tax liability.

3. Flexible Spending Rules

The "fixed withdrawal" model—where a retiree takes the same amount regardless of market performance—is a recipe for depletion during a crash. ProjectionLab’s "Flex Spending" feature allows users to codify their behavioral responses to market volatility. Users can set conditional rules, such as: “If the market drops 30% from all-time highs, reduce discretionary spending by 60%.” This feature provides a more realistic, stress-tested view of retirement sustainability.

4. Scenario Comparison

The upgraded "Compare Mode" acts as a sandbox for life decisions. Users can toggle variables—such as moving to a different state, accelerating a career shift to part-time work, or changing investment allocations—and visualize the impact in real-time. The ability to see the "yearly delta" in net worth and income between two competing life plans turns ambiguous decisions into data-driven choices.

Global Expansion: Beyond U.S. Borders

Recognizing that the FIRE movement is a global phenomenon, ProjectionLab has significantly broadened its scope. The platform now features dedicated support for the Canadian market, including:

- TFSA and RRSP integration.

- CPP, OAS, and GIS income estimation.

- Provincial tax presets for major regions including Ontario and Quebec.

Furthermore, the platform has expanded its reach to include localized support for the UK, Australia, the Netherlands, and Germany. This is a critical development for expatriates and those planning international retirements, as it addresses the unique tax treaties and retirement structures of these jurisdictions.

Implications for the Future of Financial Planning

The success of ProjectionLab highlights a broader shift in the financial services landscape. When asked about the impact of the software, power users often report a realization that their previous strategies were leaving hundreds of thousands of dollars on the table. In one notable instance, a user discovered that by simply adjusting their tax-deferred contribution strategy and fine-tuning their conversion timeline, they could leave over $1.5 million more to their heirs.

This is the "power of the tool"—not just to provide a forecast, but to actively improve the outcome.

A New Standard of Transparency

By remaining independent and avoiding the "advisory upsell," ProjectionLab represents a clean break from the traditional financial industry. Users are not being sold products; they are being provided with an engine to optimize their own assets. As the platform continues to iterate, the implications for the FIRE community are clear: high-level financial engineering is no longer a luxury for the ultra-wealthy.

Conclusion: Taking Control of the Path

Whether you are in the "accumulation phase"—aggressively saving and seeking tax-efficient growth—or the "decumulation phase," where the goal is to extract maximum value from your assets while minimizing tax drag, ProjectionLab offers a comprehensive solution.

The evolution of the platform over the last two years has moved it from a hobbyist’s project to a professional-grade analytical powerhouse. For those interested in testing their own assumptions, the platform remains accessible, with a free tier that allows for the creation of comprehensive plans, and a paid tier that unlocks the full suite of optimization, tax modeling, and scenario analysis tools.

In an era of economic uncertainty, having a clear, data-backed plan is the ultimate hedge. As Kyle and his team continue to innovate, one thing is certain: the bar for what we expect from our personal finance tools has been permanently raised.